Introduction

Withdrawing your Provident Fund (PF) has become faster, simpler, and more structured. The introduction of EPFO 3.0 has transformed the entire process by reducing complexity and improving digital access. At the same time, the system now ensures that you retain a portion of your savings for retirement, which is a very important financial discipline.

If you plan to withdraw your PF, you should first understand the latest rules, limits, process, and precautions. This article explains everything in clear, professional, and layman-friendly language.

You can apply through the official portal of Employees’ Provident Fund Organisation:

https://www.epfindia.gov.in/site_hi/index.php

Latest Changes in PF Withdrawal

1. Simplified Withdrawal Categories

Earlier, EPFO allowed withdrawal under multiple specific conditions. However, now it has simplified them into three broad categories:

- Essential Needs – medical treatment, education, marriage

- Housing Needs – purchase, construction, home loan repayment

- Special Circumstances – natural disasters or financial hardship

As a result, you can now choose the correct option easily without confusion.

2. Mandatory Balance Retention

One of the biggest changes is:

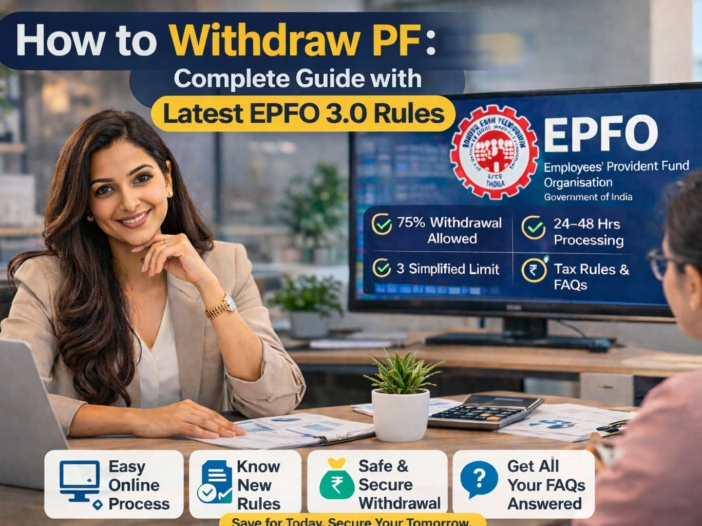

- You can withdraw up to 75% of your PF balance

- You must keep at least 25% in your account

Therefore, the system ensures that you still have funds available for retirement.

3. Updated Rules for Unemployment

If you leave your job:

- After 1 month, you can withdraw up to 75%

- After 2 months, you can withdraw the remaining balance (in case of final settlement)

This change provides flexibility while maintaining financial security.

4. Pension (EPS) Withdrawal Rule

Earlier, you could withdraw pension after 2 months. Now:

- You must wait 36 months (3 years)

This rule encourages long-term savings and continuity of pension benefits.

5. Faster Digital Processing

EPFO has significantly improved its technology:

- Claims processed within 24–48 hours

- Auto-settlement up to ₹5 lakh

- Aadhaar OTP and Face Authentication

- Mobile access through UMANG app

Consequently, the entire process is now almost paperless and very quick.

6. Tax Implications (Important)

You should also understand the tax impact:

- Before 5 years of service

→ 10% TDS (with PAN)

→ 20% TDS (without PAN) - After 5 years

→ Withdrawal is tax-free

Additionally, you can submit Form 15G/15H to avoid TDS if eligible.

Step-by-Step Process to Withdraw PF

Now, let’s understand the practical steps you should follow:

Step 1: Login to EPFO Portal

First, visit the EPFO website and log in using your UAN and password.

Step 2: Verify KYC Details

Next, ensure that your:

- Aadhaar

- PAN

- Bank account

are correctly linked and verified.

Step 3: Navigate to Claim Section

Then, go to:

Online Services → Claim (Form 31, 19, 10C)

Step 4: Verify Bank Account

After that, enter and confirm your bank account details.

Step 5: Select Claim Type

Now, choose the appropriate option:

- Full withdrawal

- Partial withdrawal

- Pension withdrawal

Step 6: Enter Details

Subsequently, fill in:

- Reason for withdrawal

- Amount required

Step 7: Complete OTP Verification

Then, authenticate using Aadhaar OTP.

Step 8: Submit and Track

Finally, submit your claim and track the status online.

Common Mistakes to Avoid

Even though the process is simple, many people make avoidable errors.

1. Not Updating KYC

If your Aadhaar or bank details are incorrect, your claim may get rejected.

2. Choosing the Wrong Category

You should always select the correct withdrawal category to avoid delays.

3. Entering Incorrect Bank Details

Even a small mistake can result in payment failure.

4. Ignoring Tax Rules

If you withdraw before 5 years, you may face tax deductions.

5. Withdrawing Without Planning

Although you can withdraw up to 75%, you should avoid unnecessary withdrawals.

Important FAQs

1. Can I withdraw full PF anytime?

No. You can generally withdraw up to 75%, except in cases like retirement or final settlement.

2. How long does it take to receive PF?

Usually, it takes 24–48 hours to 5 days, depending on verification.

3. Is Aadhaar mandatory?

Yes. Aadhaar linking is essential for online withdrawal.

4. Can I withdraw PF while working?

Yes, but only partial withdrawal for valid reasons.

5. Is PF withdrawal taxable?

- Before 5 years → taxable

- After 5 years → tax-free

6. Can I withdraw PF multiple times?

Yes, but only under allowed categories and conditions.

7. What happens if my claim is rejected?

You should correct the issue (KYC, bank, or details) and apply again.

8. Do I need employer approval?

In most online cases, employer approval is not required.

9. Can I track my PF claim?

Yes, you can track it under “Track Claim Status” on the portal.

10. What is the minimum balance rule?

You must retain at least 25% of your PF balance.

Conclusion

In conclusion, PF withdrawal in 2026 is efficient, digital, and user-friendly. While EPFO 3.0 simplifies the process, it also promotes financial discipline by protecting your retirement savings.

Therefore, you should always:

- Keep your KYC updated

- Choose the correct withdrawal type

- Plan your withdrawal carefully

By following these steps, you can ensure a smooth and hassle-free PF withdrawal experience.