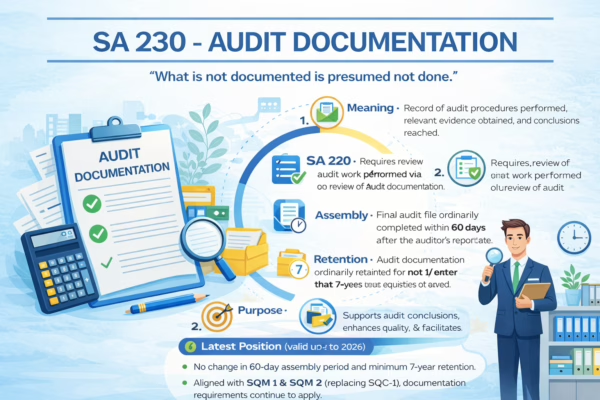

Introduction Audit documentation plays a critical role in the audit process. It not only supports the auditor’s opinion but also demonstrates that the audit was conducted in accordance with applicable Standards on Auditing (SAs) and legal requirements.SA 230 – Audit Documentation prescribes the auditor’s responsibility to prepare audit documentation that provides a sufficient and appropriate […]

Uncategorized

SA 220 – Quality Control for an Audit of Financial Statements

Introduction Quality is the backbone of any audit. SA 220 focuses on ensuring that every audit engagement is performed with due care, competence, and compliance. It guides auditors on how to apply quality control policies at the individual audit level, while aligning with the firm’s overall quality framework. Objective of SA 220 The primary objective […]

SA 210: Agreeing the Terms of Audit Engagements

SA 210 – Agreeing the Terms of Audit Engagement SA 210 – Agreeing the Terms of Audit Engagement explains the process of formally agreeing on the terms of audit between the auditor and the client. It requires the auditor to agree these terms through an audit engagement letter. This letter acts like a written agreement […]

SA 200 – Overall Objectives of the Independent Auditor

Objective of SA 200 SA 200 explains the overall objectives of the independent auditor and sets out the nature and scope of an audit. It also establishes the auditor’s responsibility to comply with Standards on Auditing (SAs) while performing an audit. Overall Objectives of the Auditor The auditor aims to: Obtain reasonable assurance about whether […]

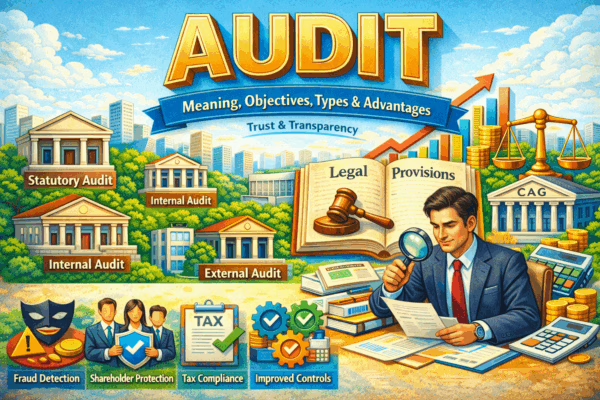

What is Audit and Types of Audit

Introduction In today’s business environment, organizations carry out many financial transactions that affect investors, lenders, government authorities, and other stakeholders. These stakeholders rely on financial statements to make important economic decisions. Therefore, it is essential that financial information is accurate and reliable. Audit helps in achieving this by independently examining financial records and statements. It […]