Introduction

Audit documentation plays a critical role in the audit process. It not only supports the auditor’s opinion but also demonstrates that the audit was conducted in accordance with applicable Standards on Auditing (SAs) and legal requirements.

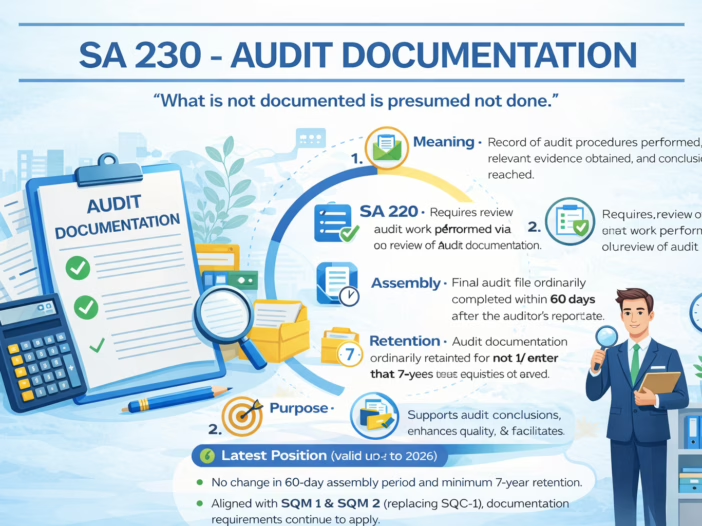

SA 230 – Audit Documentation prescribes the auditor’s responsibility to prepare audit documentation that provides a sufficient and appropriate record of the basis for the auditor’s report.

Meaning of Audit Documentation

Audit documentation refers to the record of audit procedures performed, relevant audit evidence obtained, and conclusions reached by the auditor.

According to SA 230, audit documentation that meets the requirements of this SA and other relevant SAs provides:

-

Evidence of the auditor’s basis for a conclusion about the achievement of the overall objectives of the audit; and

-

Evidence that the audit was planned and performed in accordance with Standards on Auditing and applicable legal and regulatory requirements.

Thus, audit documentation acts as proof of both work done and professional judgment applied.

Nature and Purpose of Audit Documentation

Audit documentation serves multiple purposes. First, it supports the auditor’s report. Second, it enhances audit quality.

More specifically, audit documentation:

-

Records audit procedures performed

-

Captures relevant audit evidence obtained

-

Documents conclusions reached by the auditor

Further, preparing sufficient and appropriate audit documentation on a timely basis helps to:

-

Enhance the quality of audit work

-

Facilitate effective review and supervision

-

Enable proper evaluation of audit evidence and conclusions before finalizing the auditor’s report

Documentation of Significant Matters

SA 230 requires the auditor to document discussions of significant matters with:

-

Management

-

Those charged with governance

-

Others, where relevant

The auditor must record:

-

The nature of significant matters discussed

-

When the discussions took place

-

With whom the discussions were held

This documentation strengthens accountability and supports professional judgment exercised during the audit.

Completion Memorandum (Summary of Significant Matters)

In addition, the auditor may consider preparing and retaining a completion memorandum.

This memorandum:

-

Describes significant matters identified during the audit, and

-

Explains how those matters were addressed

A completion memorandum helps in summarizing key audit issues and supports the final audit conclusion.

Review of Audit Documentation

SA 220 requires the auditor to review audit work performed through a review of audit documentation.

This review ensures that:

-

Audit procedures were properly performed

-

Conclusions are consistent with evidence obtained

-

Work complies with applicable Standards on Auditing

Thus, audit documentation becomes the primary tool for quality control at the engagement level.

Assembly of the Final Audit File

The auditor must complete the assembly of the final audit file within an appropriate time period after the date of the auditor’s report.

As per SA 230:

-

The ordinary time limit is not more than 60 days from the date of the auditor’s report

After this period, the auditor must not delete or discard audit documentation before the end of its retention period.

Retention of Audit Documentation

Audit firms are required to establish policies and procedures for the retention of engagement documentation.

Ordinarily, the retention period for audit engagements is no shorter than 7 years from the date of the auditor’s report, or longer if required by law or regulation.

This requirement ensures availability of audit evidence for:

-

Regulatory inspections

-

Peer review

-

Legal or disciplinary proceedings

Working Papers – The Backbone of Audit Documentation

Audit documentation is commonly referred to as working papers.

These working papers:

-

Provide evidence of audit work performed

-

Support audit conclusions

-

Assist in future audits and reviews

Hence, well-maintained working papers reflect the professional competence and diligence of the auditor.

Latest Position Valid up to 2026

-

SA 230 remains unchanged in core principles up to 2026

-

Quality control requirements now align with SQM 1 and SQM 2 (replacing earlier SQC-1), but documentation requirements under SA 230 continue to apply fully

-

The 60-day assembly rule and minimum 7-year retention period continue to be valid

Conclusion

In conclusion, SA 230 emphasizes that “what is not documented is presumed not done.”

By maintaining clear, complete, and timely audit documentation, the auditor demonstrates compliance with auditing standards, supports audit conclusions, and enhances audit quality.

Proper audit documentation is not merely a procedural requirement—it is the foundation of a credible and defensible audit.