Introduction SA 402 applies when an entity uses a service organisation to perform functions that are relevant to financial reporting. These services may include payroll processing, cloud accounting, IT infrastructure, data management, or transaction processing. This Standard explains how the auditor applies SA 315 (Identifying and Assessing the Risks of Material Misstatement) and SA 330 […]

Companies Act

SA 330 – The Auditor’s Responses to Assessed Risks

Introduction SA 330 requires the auditor to respond appropriately to the risks of material misstatement identified during the audit. After assessing risks, the auditor must design and perform audit procedures that directly address those risks and obtain sufficient appropriate audit evidence. Objective of SA 330 The auditor aims to obtain sufficient and appropriate audit evidence […]

SA 320 – Materiality in Planning and Performing an Audit

Introduction SA 320 explains how an auditor applies the concept of materiality while planning and performing an audit of financial statements. In simple words, materiality means the size of an error or misstatement that can influence the decisions of users of financial statements. If an error is big enough to affect decisions, we treat it […]

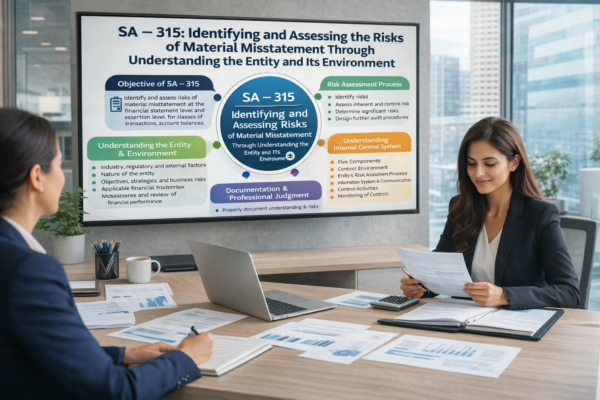

SA – 315: Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

Introduction SA – 315 deals with the auditor’s responsibility to identify and assess the risks of material misstatement in the financial statements. Before performing detailed audit procedures, the auditor must understand: The entity Its environment The applicable financial reporting framework The entity’s system of internal control This understanding provides a strong foundation for designing further […]

SA 300 – Planning an Audit of Financial Statements

Introduction SA 300 deals with the planning of an audit of financial statements. Planning is a critical stage of the audit process. The auditor must plan the audit so that it is performed in an effective and efficient manner. Proper planning helps identify significant risk areas, allocate resources appropriately, and ensure compliance with Standards on […]