Section 194A of Income Tax Act deals with TDS On Interest U/s 194A on Interest other than interest on securities.

On which income section 194A is applicable?

It is applicable on interest other than interest on securities. It covers interest received from banks, post office, cooperative society.

It excludes interest on securities. Securities means shares, debentures of a company.

What is TDS rate under section 194A?

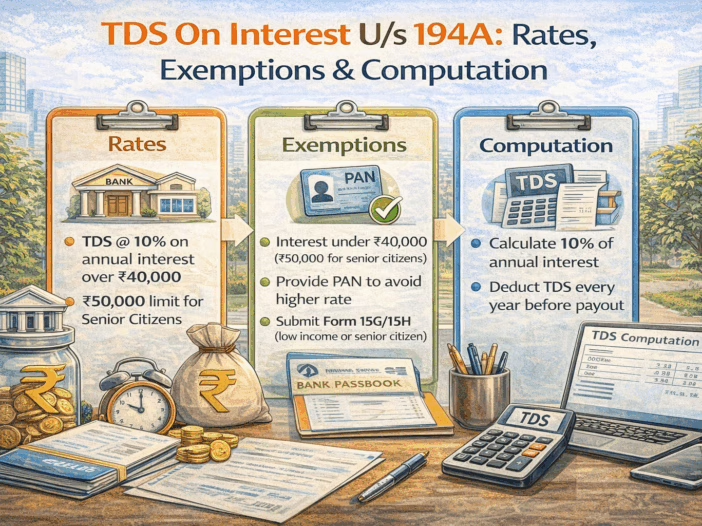

Rate of TDS: The standard rate for TDS under Section 194A is 10% of the interest amount, provided the payee’s Permanent Account Number (PAN) is available. If the PAN is not provided, TDS is deducted at a higher rate of 20%.

What is TDS limit under section 194A?

Rs. 10,000 limit

TDS is deductible if the interest amount exceeds Rs 10,000 during the financial year.

Rs. 40,000 Limit

However, in below cases if such interest is paid by the following entities, tax shall not be deducted at source unless the payment exceeds Rs50,000.

- A banking company

- Post office on any deposit under any scheme framed and notified by central gov.

- A cooperative society engaged in banking business only if the total sales/gross receipts/turnover of the co-operative society exceeds 50 crore rupee during the FY immediately preceding the FY in which interest is credited or paid (amendment by Finance Act 2020)

- For Example, if you earn interest on Fixed deposit more than Rs. 50,000, then the bank will deduct TDS @10% on whole Interest amount.

- Suppose, if you earn interest of Rs. 55000 from your fixed deposit with bank, the TDS deducted will be Rs. 5,500.

Rs. 100,000 limit

In case interest is received by senior citizen, then TDS limit to deduct TDS under section 194A is Rs. 100,000.

Comparative Chart of TDS Exemption Limits Under Section 194A

| Category of Payer | FY 2020-21 to FY 2024-25 | FY 2025-26 (Revised) | Change |

| Banking Companies (Banks, Post Office, Cooperative Banks) – For Senior Citizens (60+ years) | ₹50,000 | ₹1,00,000 | Increased |

| Banking Companies (Banks, Post Office, Cooperative Banks) – For Other Individuals | ₹40,000 | ₹50,000 | Increased |

| Cooperative Societies Engaged in Banking | ₹40,000 (₹50,000 for Senior Citizens) | ₹50,000 (₹1,00,000 for Senior Citizens) | Increased |

| Non-Banking Payers (Companies, NBFCs, Others) | ₹5,000 | ₹5,000 | No Change |

TDS Rates Under Section 194A

| Condition | TDS Rate |

| If PAN is Available | 10% |

| If PAN is Not Available | 20% |

Whether section 194A provisions applicable on individual and HUF?

This section is applicable to all persons. But for Individual/HUF it is liable to deduct TDS ON INTEREST under section 194A only if their sales, gross receipt turnover exceeds one crore rupees in case of business or fifty lakh rupees in case of profession in the immediately preceding financial year [Section 44AB].

What is the time of deduction u/s 194A?

As per Section 194A of the Income Tax Act, 1961, TDS on interest (other than interest on securities) must be deducted at the earlier of the following two events:

- At the time of credit of interest to the account of the payee (even if it is credited to a suspense account or any other account).

- At the time of actual payment of interest (in cash, cheque, draft, or any other mode).

This means that even if interest is not paid in cash but is accrued and credited to an account, TDS must still be deducted.

Example:

- If interest of ₹50,000 is credited to a depositor’s account on 31st March 2025, but the actual payment is made on 15th April 2025, then TDS must be deducted on 31st March 2025 (the date of credit).

- If the interest is paid in cash on 15th April 2025, and no prior credit entry was made, then TDS must be deducted on 15th April 2025 (date of payment).

Time of crediting interest or Time of payment in cash or any other mode whichever is earlier

[The account to which the interest is credited may be any name eg- “suspense account” or “Interest payable account”.

How to Claim a Refund of TDS Deducted Under Section 194A?

If excess TDS has been deducted on interest income under Section 194A, you can claim a refund by filing an Income Tax Return (ITR). Follow the step-by-step guide below:

📌 Step 1: Check Your TDS Deduction in Form 26AS & AIS

- Log in to the Income Tax e-Filing portal: https://www.incometax.gov.in

- Download Form 26AS and Annual Information Statement (AIS) to verify the TDS deducted under Section 194A.

- Ensure that the TDS deducted matches the interest income earned.

📌 Step 2: Determine If You Are Eligible for a TDS Refund

You can claim a TDS refund if:

✅ Your total income is below the taxable limit (₹2.5 lakh for individuals, ₹3 lakh for senior citizens, ₹5 lakh for super senior citizens).

✅ The bank/NBFC/post office deducted TDS even though your total income is non-taxable.

✅ You submitted Form 15G/15H, but TDS was still deducted.

✅ You fall under the new exemption limits for FY 2025-26 (₹1,00,000 for senior citizens, ₹50,000 for others).

📌 Step 3: File an Income Tax Return (ITR)

To claim a refund, filing an ITR is mandatory, even if your income is below the taxable limit.

Choose the Correct ITR Form

- ITR-1 (Sahaj) – If you have only salary, pension, and interest income.

- ITR-2 – If you have other sources of income (e.g., capital gains).

Steps to File ITR Online for TDS Refund

1 .Log in to the Income Tax e-Filing Portal.

2 .Click on ‘File Income Tax Return’ → Select AY 2025-26.

3 .Choose ITR-1 or ITR-2 based on your income type.

4 .Under “Income Details”, enter total interest income (from FDs, RDs, etc.).

5 .Check TDS credit details (it should match Form 26AS & AIS).

6 .The system will automatically calculate the refund if excess TDS was deducted.

7 .Enter your bank account details for refund processing.

8 .Validate & Submit the return.

📌 Step 4: Verify the ITR

After submitting the ITR, you must verify it to process your refund:

- E-Verify (Instant Method) – Use Aadhaar OTP, Net Banking, or Digital Signature (DSC).

- Physical Verification (Manual Method) – Download ITR-V, sign it, and send it to CPC Bengaluru within 120 days.

📌 Step 5: Track Refund Status

- 1. Log in to the Income Tax Portal.

2. Click on ‘Refund/Demand Status’.

3. If the refund is approved, it will be credited to your bank account within 30-45 days.

📌 Example: TDS Refund Calculation

| Details | Amount (₹) |

| Interest Income (Fixed Deposit) | 60,000 |

| TDS Deducted (10% u/s 194A) | 6,000 |

| Other Taxable Income | 1,50,000 |

| Total Income (Exempt Limit ₹2,50,000) | 2,10,000 |

| Tax Liability | 0 (Below Exemption) |

| Refund Due | 6,000 |

Since the total income is below the taxable limit, you can claim a full refund of ₹6,000.

📌 Frequently Asked Questions (FAQs)

1. When will I get my TDS refund?

Refunds are usually processed within 30-45 days from the date of ITR processing by the IT Department.

2. Can I claim a refund if I forgot to submit Form 15G/15H?

Yes, file an ITR and claim the excess TDS as a refund.

3. What if I do not file an ITR for my TDS refund?

If you do not file an ITR, the excess TDS deducted will not be refunded automatically.

4. Can I track my TDS refund online?

Yes, track your refund at https://www.incometax.gov.in under ‘Refund/Demand Status’.

What is the exemptions from TDS on Interest?

- Exemptions has been granted from the deduction of tax at source (TDS ON INTEREST 194A) in respect of the following:

- Interest credited or pay by a firm to a partner of the firm

- Interest credited or paid by a cooperative society to its member or to any other co-operative society

- Interest on the compensation amount awarded by the motor accident claims tribunal where the aggregate of such interest income in financial year does not exceed Rs 50,000;

- Income paid or payable at income coupon bonds issued by an infrastructure capital company or infrastructure capital fund or a public sector company or a scheduled bank;

- Interest paid to banking company or any cooperative society engaged in banking business

- Interest paid to financial corporation established under a central, state or provincial act;

- Interest paid to LIC, UTI, any company or cooperative society carrying on insurance business;

- Interest on deposits with a banking company other than time deposit;

- Income credited or paid in respect of deposits under any scheme framed by central government;

- Income paid or credited in respect of deposits with:-

- A primary agricultural credit society or a primary credit society or a cooperative land mortgage bank or a co-operative land development bank

- Deposits other than time deposits, with a cooperative society carrying on banking business, other than a co-operative society, referred above.

- Interest credited or paid by central government under income tax act, 1961 and wealth tax act, 1957, viz, interest on refunds.

Important points under section 194A

- Section 194A is applicable only to interest paid/credited to residents

- Senior citizen means a resident individual whose age is 61 or more during the relevant Previous Year

- The term “time deposit” includes recurring deposit

- If you believe that your income will not exceed the minimum income chargeable to tax, then you can submit 15CA/15CB to the bank and on such submission the bank will not deduct any TDS.₹10,000 – For other cases (like interest from companies, NBFCs, etc.)

FAQs on TDS on Interest (Section 194A)

Here are some frequently asked questions (FAQs) related to TDS on Interest under Section 194A of the Income Tax Act, 1961:

- What is TDS On Interest U/s 194A of the Income Tax Act?

Ans: Section 194A mandates the deduction of Tax Deducted at Source (TDS) on interest (except interest on securities) paid to residents if the amount exceeds prescribed thresholds.

- Who is required to deduct TDS under Section 194A?

Ans: Any person (other than an individual or HUF) who is responsible for paying interest to a resident must deduct TDS. However, individuals and HUFs must deduct TDS if their business turnover exceeds ₹1 crore or professional receipts exceed ₹50 lakh in the preceding financial year.

- What is the rate of TDS On Interest U/s 194A under Section 194A?

Ans: The TDS rate is 10% if the recipient provides a valid PAN. If the recipient does not provide PAN, TDS is deducted at 20%.

- What are the threshold limits for TDS deduction under Section 194A?

Ans:

- ₹40,000 – Interest paid by banks, post offices, and cooperative banks (for non-senior citizens).

- ₹50,000 – Interest paid by banks, post offices, and cooperative banks (for senior citizens).

- ₹5,000 – Interest paid by other entities (like companies, NBFCs, etc.).

- When should TDS be deducted under Section 194A?

Ans:

TDS should be deducted at the earlier of:

- The date of crediting the interest to the payee’s account (even if credited to a suspense account).

- The date of actual payment of interest (whichever is earlier).

- Who is exempt from TDS under Section 194A?

Ans: No TDS is required if:

✅ Interest is paid to banks, LIC, UTI, or the Government.

✅ Cooperative societies pay interest to their members.

✅ Senior citizens submit Form 15H (if total income is below the taxable limit).

✅ Other individuals submit Form 15G (if income is below the basic exemption limit).

✅ Interest paid by a partnership firm to its partners.

- Is TDS deducted on savings account interest?

Ans: No, Section 194A applies only to interest other than interest on securities, so savings account interest is not subject to TDS.

- How can individuals avoid TDS deduction on their interest income?

Ans: By submitting:

- Form 15G (for individuals below 60 years) if total taxable income is below the exemption limit.

- Form 15H (for senior citizens above 60 years) if tax liability is nil.

- What is the due date for depositing TDS under Section 194A?

Ans:

- For non-government deductors – 7th of the next month (except March, which is 30th April).

- For government deductors – Same day as payment if paid by book adjustment; otherwise, 7th of the next month.

- What is the penalty for not deducting or depositing TDS on time?

Ans:

❌ Interest on late deduction – 1% per month from the date TDS was deductible to the actual deduction date.

❌ Interest on late deposit – 1.5% per month from the deduction date to the actual deposit date.

❌ Penalty under Section 271C – Equal to the amount of TDS not deducted/deposited.

❌ Disallowance under Section 40(a)(ia) – The expense (interest payment) may be disallowed while calculating taxable income.

- Is TDS under Section 194A applicable to cooperative societies?

Ans:

- Yes, if the cooperative society’s total sales, turnover, or gross receipts exceeded ₹50 crore in the preceding financial year.

- If the society qualifies, it must deduct TDS on interest exceeding ₹40,000 (₹50,000 for senior citizens).

- Can a person claim a refund of excess TDS deducted under Section 194A?

Ans: Yes, if TDS has been deducted but the taxpayer’s total income is below the taxable limit, they can file an income tax return (ITR) and claim a refund of the excess TDS.